Employees' Retirement System

-

The New York State and Local Retirement System (NYSLRS), also known as the Employees' Retirement System (ERS), provides service and disability retirement benefits, as well as death benefits to employees of participating public employers in non-teaching positions.

-

What is NYSLRS?

NYSLRS is the third largest retirement system in the nation, with more than 1.1 million members, retirees and beneficiaries. State Comptroller Thomas P. DiNapoli administers the Retirement System and is trustee of the New York State Common Retirement Fund, which holds and invests NYSLRS assets. The Fund had a value of $210.5 billion as of March 31, 2019.

-

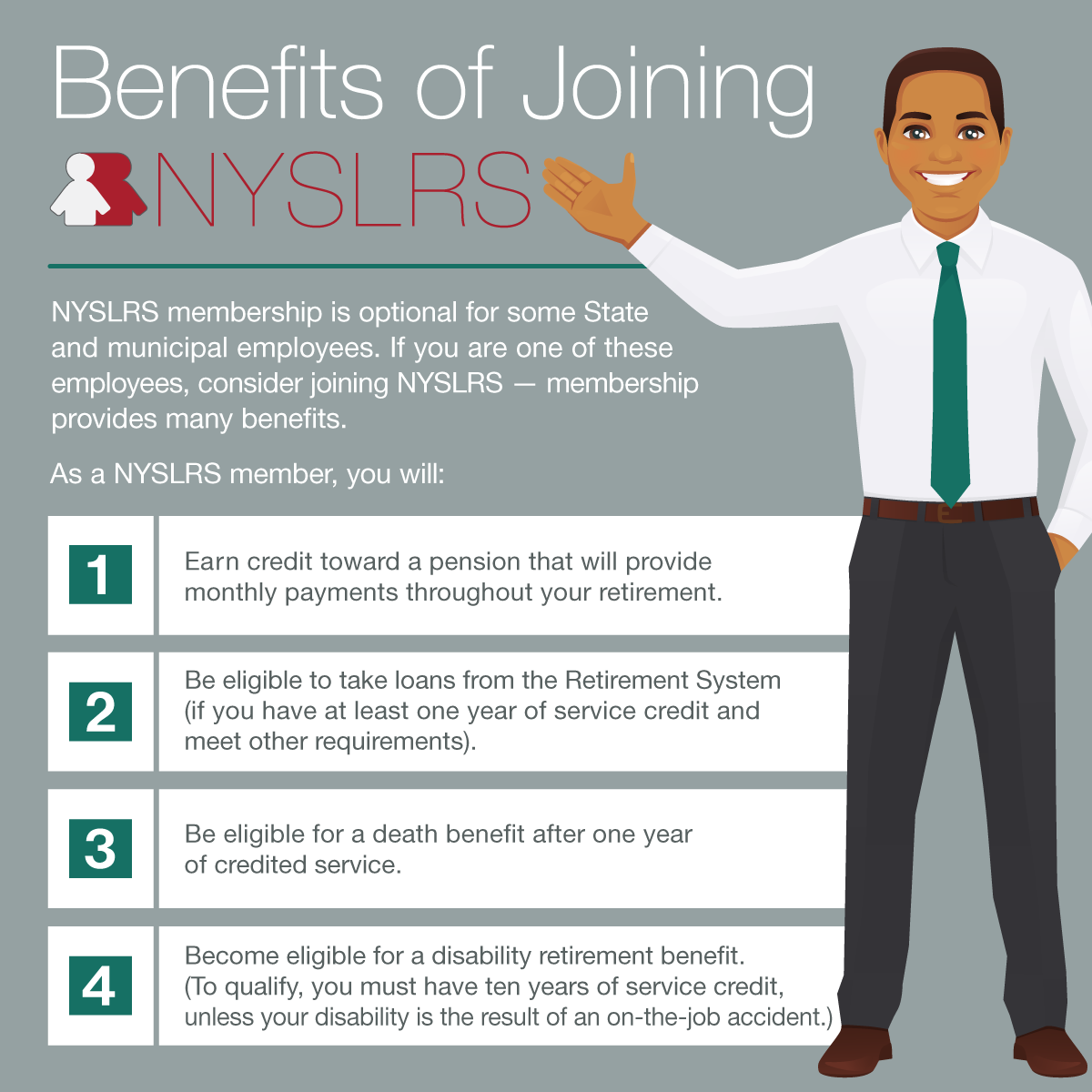

Should You Join NYSLRS?

Most State and municipal employees are required to join the New York State and Local Retirement System (NYSLRS) when they are hired. But for some employees, such as part-time and seasonal workers, membership is optional.

Joining NYSLRS will improve your chances of a secure financial future. You’ll earn credit toward a pension that will provide monthly payments throughout your retirement. But NYSLRS also provides other important benefits such as death benefits, disability benefits and the ability to take a loan against your contribution amounts.

-

What Does NYSLRS Offer?

As a NYSLRS member, you’ll be eligible for a pension after you earn ten years of service credit. (This is called being vested.) If you work part-time, service credit is pro-rated. For example, if you work half of the hours that a full-time employee works, you’ll receive six months credit for every year you work.

Also, as a NYSLRS member you’ll be able take loans from your contributions if you’ve earned a year of service credit and meet other requirements. You’ll be eligible for a death benefit once you have one year of service credit, and disability benefits after you have ten years of service credit. (If your disability results from an on-the-job accident, not due to your own willful negligence, there is no minimum service requirement.)

Over 3,000 employers participate in NYSLRS, allowing you to continue to build on your benefits if you go to work for another government employer. Your benefits also may be transferable to six other public retirement plans in New York.

-

Making Contributions

You’ll contribute between 3 and 6 percent of your earnings to the Retirement System. Contribution rates vary based on each member’s annual compensation. If you don’t join NYSLRS when you first start working and later decide to purchase your previous service credit, you will need to contribute 6 percent of those earnings plus interest, even if your salary level for the prior time period would have resulted in a lower contribution rate.

Your NYSLRS pension will be based on your service credit and salary, not on the amount you contribute. A NYSLRS pension is a lifetime benefit. Unlike a 401-k, there is no risk that your pension benefits will be reduced during your retirement.

But what if you join NYSLRS and decide to leave public service before you are vested? You won’t lose your contributions. In fact, you can withdraw your accumulated contributions, plus interest, and roll that money into a retirement savings plan at your new job.

-

How School Employees Earn Service Credit

As a member, you receive service credit for paid public employment beginning with your date of membership. That credit is based on the number of days you work, which your employer reports to us.

If you’re working full-time, you receive one year of service per school year, even if you only work 10 months of the year.

For part-time work, your employer calculates days worked by dividing the number of hours worked by the hours in a full-time day. The number of hours in a full-time day is set by your employer (between six and eight hours). So, for example, if a 40-hour work week is considered full-time for your employer, and you work 20 hours a week for a given school year, you will receive half a year of service credit.

-

Check Your Service Credit

You can sign in to Retirement Online and find your current estimated service credit listed on your Account Homepage under ‘My Account Summary.’

If you’re not sure whether you’re earning full-time or part-time service, you can check your most recent Member Annual Statement to see how much service you earned over the past fiscal year. To view your most recent Statement, sign in to Retirement Online. From your Account Homepage, click the “View My Member Annual Statement” button under ‘My Account Summary.’ If you are receiving full-time service, it will say “1.00 Years” for service credited from 4/1/2022 – 3/31/2023. A reminder: the total credited service you will see listed on your Statement was as of March 31, 2023.

-

SCAM ALERT 12/3/24

NYSLRS is monitoring a potential cyber threat involving Retirement Online. Scammers have created a fake website, which looks similar to Retirement Online, aimed to trick users and capture login credentials. Click here for more information.